As your ESOP matures, you may feel that you and your employees are starting to better understand your plan provisions and the benefits an ESOP provides. It is important for participants to feel engaged and knowledgeable about their plan. One item that can be difficult to communicate to your employees and comes later in the ESOP’s development is diversification. Your participants will want to know when they can diversify, how much they can diversify, and what their diversification withdrawal options are.

As your ESOP matures, you may feel that you and your employees are starting to better understand your plan provisions and the benefits an ESOP provides. It is important for participants to feel engaged and knowledgeable about their plan. One item that can be difficult to communicate to your employees and comes later in the ESOP’s development is diversification. Your participants will want to know when they can diversify, how much they can diversify, and what their diversification withdrawal options are.

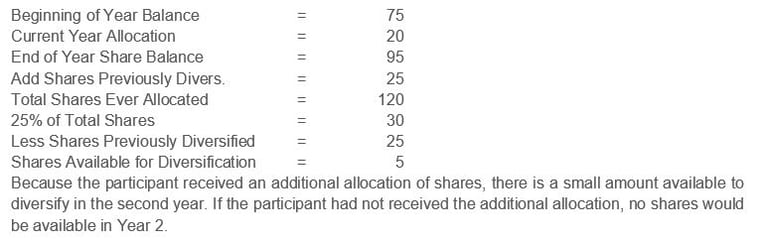

You are required to offer diversification to participants who have reached age 55 and 10 Years of Participation (YOP). Your Plan Document will specify what constitutes a Year of Participation for Diversification – it may be different than Years of Service for Vesting and Eligibility. In the first five years that a participant is eligible for diversification, they can diversify up to 25% of the shares ever allocated to their account, reduced by any shares previously diversified. Many participants will assume that they can withdraw 25% of their balance each year, however as laid out in the example below, the formula is more complicated than that. If a participant elects to receive the full 25% allowable in the first year and no additional shares are allocated to their account, they will not be able to diversify again until the sixth and final year. This often surprises participants who expect a similar diversification amount each year. In the sixth year, the amount available for diversification increases to 50% of all shares ever allocated to that participant (less any shares previously diversified). Once eligible to diversify, participants will need to decide whether to rollover their distribution to another qualified plan, or take the distribution as a taxable distribution (or a combination of both). Participants should be informed of the tax implications (and potential penalties) if they decide not to rollover their diversification. Some plans may satisfy diversification requirements through a transfer to the company’s 401(k) plan, or by offering at least three investment options within the plan. Diversification is voluntary, so participants always have the option to decline diversification and leave their shares in their account. They can also choose to diversify less than the maximum number of shares available for that year. A participant must make a separate election each year. Certain factors may complicate the diversification determinations. Depending on your plan provisions, a participant may be eligible for both diversification and a distribution after terminating employment. If your plan segregates terminated employees out of company stock, this will affect the amounts available for diversification. Plans may also limit diversification to active employees. Your administrator will be able to discuss how diversification will work specifically for your plan, and point out any potential issues to consider. We recommend starting to plan early for diversification and how to explain this feature to your participants. Depending on your company culture, webinars, small groups, or handouts may be the best option to educate participants about diversification options in the future. Familiarize yourself with your plan document, and remember that your plan administrator is available for any questions.

Sample diversification timing for a participant who attained age 55 and 10 YOP in 2016:

Sample Diversification Calculation:

Year 1

Year 2

Please note, this overview focuses on the minimum requirements for statutory diversification. Your specific plan provisions may vary.